S-1/A: General form of registration statement for all companies including face-amount certificate companies

Published on August 4, 2008

Table of Contents

As filed with the Securities and Exchange Commission on August 4, 2008

Registration No. 333-150224

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CODEXIS, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 8731 | 71-0872999 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

200 Penobscot Drive, Redwood City, CA 94063

(650) 421-8100

(Address, including zip code, and telephone number, including area code, of Registrants principal executive offices)

Alan Shaw, Ph.D.

President and Chief Executive Officer

Codexis, Inc.

200 Penobscot Drive, Redwood City, CA 94063

(650) 421-8100

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Patrick A. Pohlen Latham & Watkins LLP 140 Scott Drive, Menlo Park, CA 94025 Telephone: (650) 328-4600 Facsimile: (650) 463-2600 |

Douglas T. Sheehy Vice President and General Counsel Codexis, Inc. 200 Penobscot Drive Redwood City, CA 94063 Telephone: (650) 421-8100 Facsimile: (650) 421-8102 |

John A. Fore Michael S. Russell Wilson Sonsini Goodrich & Rosati, Professional Corporation 650 Page Mill Road Palo Alto, CA 94304 Telephone: (650) 493-9300 Facsimile: (650) 493-6811 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of large accelerated filer, accelerated filer and smaller reporting company in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer ¨ | |

| Non-accelerated filer (Do not check if a smaller reporting company) x |

Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee |

||

| Common Stock, $0.0001 par value |

$100,000,000 | $3,930(2) | ||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933. |

| (2) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information contained in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED AUGUST 4, 2008

Shares

Codexis, Inc.

Common Stock

Prior to this offering, there has been no public market for our common stock. We anticipate that the initial public offering price will be between $ and $ per share. We have applied to list our common stock on The Nasdaq Global Market under the symbol CDXS.

We are selling shares of our common stock.

The underwriters have an option to purchase a maximum of additional shares from us to cover over-allotments of shares.

Investing in our common stock involves risks. See Risk Factors beginning on page 9.

| Price to Public | Underwriting Discounts and Commissions |

Proceeds to Codexis |

|||||||

| Per Share |

$ | $ | $ | ||||||

| Total |

$ | $ | $ | ||||||

Delivery of the shares of common stock will be made on or about , 2008.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse | Goldman, Sachs & Co. | |||

| Piper Jaffray | ||||

| RBC Capital Markets | ||||

| Thomas Weisel Partners LLC | ||||

The date of this prospectus is , 2008.

Table of Contents

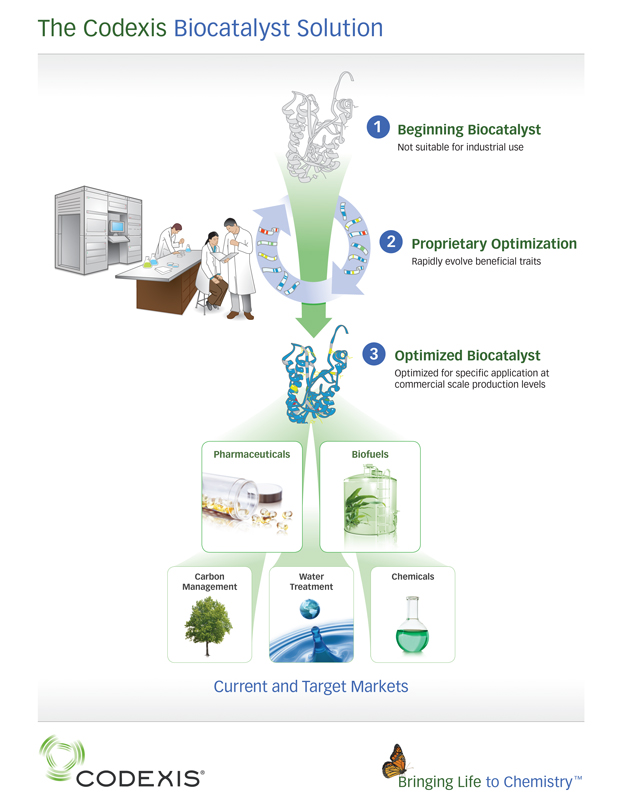

The Codexis Biocatalyst Solution

Beginning Biocatalyst

Not suitable for industrial use

Proprietary Optimization

Rapidly evolve beneficial traits

Optimized Biocatalyst

Optimized for specific application at commercial scale production levels

Pharmaceuticals

Biofuels

Carbon Management

Water Treatment

Chemicals

Current and Target Markets

CODEXIS

Bringing Life to Chemistry

Table of Contents

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date on the front cover of this prospectus, or such other dates as are stated in this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

Dealer Prospectus Delivery Obligation

Until , 2008 (25 days after commencement of this offering), all dealers that buy, sell, or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information you should consider in making your investment decision. You should read this summary together with the more detailed information, including our financial statements and the related notes, elsewhere in this prospectus. You should carefully consider, among other things, the matters discussed in Risk Factors, before making an investment decision. Unless otherwise indicated herein, Codexis, Inc., Codexis, the Company, we, us and our refer to Codexis, Inc. and its subsidiaries.

Our Company

We are a leading developer of proprietary biocatalysts that we believe have the potential to revolutionize chemistry-based manufacturing processes across a variety of industries. Our proprietary biocatalysts include existing biocatalysts that we have optimized and new biocatalysts that we have developed using our technology platform. We have focused our biocatalyst development efforts on large and rapidly growing markets, including pharmaceuticals and biofuels. We have used our technology platform to enable biocatalyst-based commercial scale drug manufacturing processes and delivered biocatalysts and drug products to some of the worlds leading pharmaceutical companies. In addition to our commercial success in the pharmaceutical industry, we have a research collaboration with Shell to apply our technology platform to the biofuels market. The commercialization of any products that may be developed through the collaborative research agreement will be at Shells discretion. We are also pursuing funded collaborations in several other bioindustrial markets, including carbon management, water treatment and chemicals.

Biocatalysts are enzymes or microbes that initiate or accelerate chemical reactions. This process, known as biocatalysis, can enable the production of products used in everyday life. Our proprietary technology platform allows us to rapidly evolve and optimize biocatalysts to perform specific and desired chemical reactions for commercial scale industrial applications. We believe we can use our technology platform to improve industrially relevant characteristics of any biocatalyst, enabling manufacturing processes that are faster, less complex, less capital intensive and lower cost than conventional chemistry-based processes. In addition, we believe that our technology platform can enable the production of products that are currently impossible to produce economically at commercial scale.

Our pharmaceutical customers have included Arch Pharmalabs Limited, Bristol-Myers Squibb Co., Dr. Reddys Laboratories Ltd., Merck & Co., Inc., Pfizer Inc., Ranbaxy Laboratories Limited, Schering-Plough Corporation and Teva Pharmaceutical Industries Ltd. In 2007, after exceeding targets related to enzyme performance under an initial one-year research agreement, we entered into a new, five-year collaborative research agreement with Equilon Enterprises LLC dba Shell Oil Products US, or Shell, to develop biocatalysts for use in producing biofuels from renewable sources of non-food sustainable plant materials, commonly known as cellulosic biomass. In the year ended December 31, 2007, we generated $25.3 million in revenues from various sources including collaborative research and development funding, product sales and government grants.

The Biocatalysis Opportunity Industry Overview

Many industries, from pharmaceuticals to energy to chemicals, use conventional chemical reactions in manufacturing processes. However, conventional chemistry-based manufacturing often requires highly complex, energy-intensive processes that use extreme environments in terms of temperature and pressure, as well as hazardous reagents to effect chemical reactions. These processes often require equipment that is expensive to build and operate, and frequently generate high volumes of waste, some of which is hazardous to health or the environment, that must be treated, contained and disposed.

Biocatalysts can enable superior alternatives to conventional chemistry in industrial applications. For example, biocatalysts can operate at or near room temperature and pressure and therefore can enable significant cost savings by using less complex manufacturing equipment. Biocatalyst-enabled processes can

1

Table of Contents

produce the same or higher quality products than conventional chemistry-based manufacturing, while reducing the risks associated with extreme manufacturing environments, without generating nearly the same level of waste.

Despite the potentially significant advantages of biocatalysts, naturally occurring biocatalysts have not achieved their full potential in industrial applications. Naturally occurring biocatalysts often require alteration of their composition in order to perform adequately under industrial manufacturing conditions or at productivity levels that would make their use in commercial scale applications economical. Some companies and researchers have tried to improve the performance of naturally occurring biocatalysts or even produce novel biocatalysts using various other methods and technologies, but to date few have had success. Moreover, for certain industrial applications, there are no known naturally occurring biocatalysts that catalyze the relevant reactions.

Our Approach to Biocatalysis

Our proprietary technology platform has the potential to dramatically transform the commercial and industrial application of biocatalysts. Our platform uses advanced biotechnology methods, bioinformatics and years of accumulated know-how to significantly expedite the process of developing customized enzymes and microbes. In the case of enzymes, we start with a diverse set of genes that encode for variations of an enzyme and recombine, or shuffle, these genes to produce new variants of the enzyme. We then evaluate these new variants to identify enzymes that exhibit improved characteristics under conditions that resemble the desired manufacturing process. ProSAR, our bioinformatics software technology, allows us to identify and quantify the potential value of beneficial mutations and distinguish them from detrimental mutations. The genes that code for improved enzyme variants are put back through this process until a highly efficient enzyme is produced that meets or exceeds targeted performance characteristics. This enzyme can then be incorporated into the actual manufacturing process, where it can reduce or eliminate costly chemical-based steps and the resulting wastes. We have also used our technology platform to improve enzymes in engineered microbes to make fermentation products. We also have a complementary technology for directed evolution of microbes, called Whole Genome Shuffling, that allows us to recombine, or shuffle, the entire genome of two or more cells to produce new variants of the microbe. Our biocatalysts can significantly improve the manufacturing of pharmaceuticals, and we believe that our technology platform may enable us to develop biocatalysts for use in producing advanced biofuels and in providing solutions to other important bioindustrial markets.

Our Target Markets and Solutions

Pharmaceuticals

We initially focused our biocatalyst development efforts on the pharmaceutical industry, before expanding our focus to include biofuels and other bioindustrial opportunities. Over the last several years, pharmaceutical companies that develop branded drugs, which we refer to as innovators, have struggled with declining operating margins resulting in large part from patent expirations for their key products. As a result, innovators are increasingly looking for opportunities to improve their operating margins by reducing their manufacturing costs and outsourcing the manufacturing of active pharmaceutical ingredients, or APIs, and components used in the manufacture of APIs, commonly known as intermediates. The rise in patent expirations has also led to rapid growth of the generics industry. Because generics manufacturers compete primarily on price, these companies are also pursuing opportunities that reduce their manufacturing costs and provide them with access to low cost sources of intermediates and APIs.

Our products and services address the needs of both innovator and generics manufacturers. For example, we have developed four enzymes that enabled significant improvements in the manufacturing process for, and reduced the cost of two key intermediates used in, the production of atorvastatin, which is the API in Lipitor. We supply Pfizer with one of these intermediates, and we supply generic atorvastatin manufacturers with the other intermediate. We are currently developing intermediates or APIs for the generic equivalents of several branded pharmaceutical products including Singulair, Nexium and Crestor. We have also developed tools,

2

Table of Contents

which we call our Codex Biocatalyst Panels, that allow innovators to screen our biocatalysts across their product pipelines and portfolios to identify desired biocatalytic activity that can then be incorporated into their drug manufacturing processes. In February 2007, Merck became the first customer for this product. Once a useful biocatalyst is identified, either through the use of our Codex Biocatalyst Panels by our customers or our in-house screening services, we can supply that biocatalyst through and to commercial scale, or we can provide further biocatalytic screening and optimization, if needed.

Biofuels

In 2006, we began exploring the application of our technology platform in biofuels. Due to underlying economic, political and environmental concerns surrounding petroleum, the world is seeking renewable alternative fuel solutions. First generation biofuel manufacturers use biocatalysts to produce biofuels such as ethanol and biodiesel at commercial scale. However, these fuels do not provide an optimal solution to the petroleum dependence problem for several reasons. For many of these manufacturers, margins are volatile as costs of key commodity inputs such as corn and natural gas are highly variable, often outpacing changes to ethanol prices. In addition, there are ethical concerns with the diversion of food crops and fertile acreage to fuel production, which has also resulted in higher food and animal feed prices.

We believe that our technology platform may enable the development of biocatalysts that can be used to produce commercially viable non-ethanol biofuel alternatives to petroleum-based fuels from cellulosic biomass. As we work on this long term goal, we also intend to work on the conversion of biomass to sugars, which could also be used for near term opportunities, such as cellulosic ethanol. Shell has the right, but not the obligation, to commercialize any technology that we may develop under the research collaboration. If Shell chooses to commercialize any biofuels products that may be developed through our collaboration, we believe that Shell, which is an affiliate of one of the worlds largest distributors of biofuels, has the resources and the infrastructure to commercialize these products on a global scale. We believe that the use of biocatalysts to transform cellulosic biomass into biofuels that have characteristics similar to current petroleum-based gasoline could address the limitations of alcohol-based fuels and could ultimately transform the liquid transportation fuels industry.

Additional Bioindustrial Opportunities

We are pursuing funded collaborations in several other bioindustrial markets, including carbon management, water treatment and chemicals. We believe that our technology platform, together with the knowledge and experience gained from our efforts in the pharmaceutical market and in our biofuels research program, will allow us to capitalize on these opportunities. We will target collaborators that are industry leaders, allowing us to leverage their competitive strengths and resources in pursuit of these opportunities.

Competitive Strengths

Our key competitive strengths are:

| | Proprietary and Disruptive Technology Platform. Our proprietary platform is potentially disruptive because it addresses the significant limitations of current approaches used to develop biocatalysts and ultimately enables biocatalytic-based processes that have substantial advantages over conventional chemistry. Our technology platform allows us to quickly develop biocatalysts suitable for commercial scale and enables the development of biocatalysts with improved performance characteristics that are rarely present in naturally occurring biocatalysts, and that we believe can enable products currently impossible to produce economically at commercial scale. |

| | Multiple Major Target Markets. We currently use our technology platform to produce biocatalysts that are used at commercial scale in both the generic and innovator pharmaceutical markets. We are working with our collaborator, Shell, to develop biocatalysts for use in producing biofuels from cellulosic biomass sources. We are also pursuing funded collaborations in several other bioindustrial markets, including carbon management, water treatment and chemicals. |

3

Table of Contents

| | Partnerships with Global Industry Leaders. We believe that our technology platform has been validated through the delivery of drug manufacturing processes or products to numerous leading pharmaceutical companies, including Arch, Merck, Pfizer and Schering-Plough. In biofuels, after an initial one-year research agreement in which we exceeded targets related to enzyme performance, we entered into a new, five-year research collaboration with Shell in 2007. |

| | Capital-Efficient Business Model. We have adopted a business model that leverages our collaborators engineering, manufacturing and commercial expertise, their distribution infrastructure and their ability to fund commercial scale production facilities. If our collaborators choose to utilize our technology to commercialize new products, we believe that this capital-efficient business model will allow us to expand into new markets without having to finance or operate large industrial facilities. During the years ended 2005, 2006 and 2007, we incurred net losses of $11.6 million, $18.7 million and $39.0 million, respectively. We believe that, without our capital-efficient business model, these losses would have been greater. |

| | Diversified and Visible Revenue Base. Our 2007 revenues were derived from the innovator and generic pharmaceuticals and biofuels markets, and consisted primarily of collaborative research and development funding, product sales and government grants. Revenues from our expected sales of generic intermediates and APIs, as well as the revenues that we expect to recognize from our five-year biofuels collaborative research agreement with Shell, should provide a high degree of visibility into our aggregate revenues for the foreseeable future. |

Strategy

Our objective is to be the leading provider of optimized biocatalytic solutions across a wide range of industries. Key elements of our strategy are as follows:

| | Expand into new bioindustrial markets. We believe that we can deploy our technology platform to transform manufacturing processes throughout various bioindustrial markets. We have a research collaboration with Shell to develop biocatalysts for use in producing commercially viable fuels from cellulosic biomass. We intend to leverage our intellectual property developed under this research collaboration to pursue other funded collaborations in non-fuel bioindustrial markets, including carbon management, water treatment and chemicals. |

| | Continue growing our pharmaceutical business. We plan to launch several new intermediates and APIs for the generic equivalents of branded pharmaceutical products, including Singulair, Nexium and Crestor, beginning in late 2008. We will also continue to aggressively market our Codex Biocatalyst Panels to pharmaceutical companies to demonstrate the capabilities of our technology platform in an effort to integrate our products and services earlier and more deeply into drug development and manufacturing processes. |

| | Enter into additional strategic collaborations. We have grown our business by collaborating with market leaders that have funded the development of and application of our technology platform in the pharmaceutical and biofuels markets. We are pursuing additional collaborations that will allow us to continue to leverage our collaborators competitive strengths and financial resources in our target markets. |

| | Continue enhancing our technology platform. We intend to continue to advance our technology platform by expanding our capabilities in microbe development and by increasing the quality of our biocatalyst libraries. Improvements in either of these areas can be applied to the development of new products in our current and target markets. |

| | Further develop our supply chain. We will continue to evaluate whether to invest in our own manufacturing capabilities or to establish long term supply contracts with additional contract manufacturers. We may also opportunistically seek to secure specialty manufacturing assets and |

4

Table of Contents

| expand existing relationships for the supply of our enzymes and key pharmaceutical APIs and intermediates. |

| | Expand our business through acquisition of new technologies, products or businesses. We will continue to evaluate opportunities to acquire or license new technologies, products or businesses that complement or expand our capabilities. We may pursue licensing and acquisition opportunities in the carbon management, water treatment and chemical markets as we seek to expand into these markets. |

Corporate Information

We were incorporated in Delaware in January 2002 as a wholly-owned subsidiary of Maxygen, Inc. In March 2002, we licensed from Maxygen our core enabling technology, which comprises advanced biotechnology methods, bioinformatics and years of accumulated know-how which we use to significantly expedite the process of developing customized enzymes and microbes. In March 2002, we also commenced operations, and in September 2002, we raised our first outside funding from venture capital investors. As of March 31, 2008, Maxygen held approximately 25% of our outstanding common stock, calculated on an as-converted basis. Our principal executive offices are located at 200 Penobscot Drive, Redwood City, CA 94063, and our telephone number is (650) 421-8100. Our website address is www.codexis.com. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider information contained on our website to be part of this prospectus.

Our logo, Codexis, Codex, Codex Biocatalyst Panel, Bringing Life to Chemistry and other trademarks or service marks of Codexis, Inc. appearing in this prospectus are the property of Codexis, Inc. This prospectus contains additional trade names, trademarks and service marks of other companies. We do not intend our use or display of other companies trade names, trademarks or service marks to imply relationships with, or endorsement or sponsorship of us by, these other companies.

5

Table of Contents

The Offering

| Common stock offered to the public |

shares (or shares if the underwriters exercise their over-allotment option in full). |

| Common stock to be outstanding after this offering |

shares (or shares if the underwriters exercise their over-allotment option in full). |

| Proposed Nasdaq Global Market symbol |

CDXS |

| Use of proceeds |

We intend to use the net proceeds from this offering for working capital and other general corporate purposes, including the costs associated with being a public company and improving our internal control over financial reporting. We may also use a portion of the net proceeds to acquire other businesses, products or technologies, including those that would enable us to seek new markets for our existing products, develop new products or increase our ability to manufacture and produce our biocatalysts. However, we do not have agreements or commitments for any specific acquisitions at this time. Please see Use of Proceeds. |

| Risk factors |

See Risk Factors elsewhere in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

The number of shares of common stock to be outstanding after this offering is based on 35,805,720 shares outstanding as of March 31, 2008 and excludes:

| | 9,820,074 shares of common stock issuable upon the exercise of options outstanding as of March 31, 2008 at a weighted average exercise price of $2.49 per share; |

| | 491,513 shares of common stock issuable upon the exercise of warrants outstanding as of March 31, 2008 at a weighted average exercise price of $3.95 per share; and |

| | shares of common stock reserved for issuance under our 2008 Incentive Award Plan, which will become effective in connection with the consummation of this offering (plus an additional 1,569,360 shares of common stock reserved for future grant or issuance under our 2002 Stock Plan as of March 31, 2008, which shares will be added to the shares to be reserved under our 2008 Incentive Award Plan upon the effectiveness of the 2008 Incentive Award Plan). |

Except as otherwise indicated, all information in this prospectus assumes:

| | the conversion of all of our outstanding shares of preferred stock into 32,330,100 shares of common stock in connection with the consummation of this offering and the related conversion of all outstanding preferred stock warrants to common stock warrants; |

| | no exercise of the underwriters over-allotment option; and |

| | the filing of our amended and restated certificate of incorporation, which will occur in connection with the consummation of this offering. |

We refer to our Series A, Series B, Series C, Series D and Series E preferred stock collectively as redeemable convertible preferred stock for financial reporting purposes and in the financial tables included in this prospectus, as more fully explained in Note 2 to our consolidated financial statements. In other parts of this prospectus, we refer to our Series A, Series B, Series C, Series D and Series E preferred stock collectively as preferred stock.

6

Table of Contents

Summary Consolidated Financial Data

The following table sets forth a summary of our historical consolidated financial data for the periods ended or as of the dates indicated. You should read this table together with our consolidated financial statements and the accompanying notes, Selected Consolidated Financial Data and Managements Discussion and Analysis of Financial Condition and Results of Operations appearing elsewhere in this prospectus. The summary consolidated financial data in this section is not intended to replace our consolidated financial statements and the accompanying notes. Our historical results are not necessarily indicative of our future results.

The following table also sets forth summary unaudited pro forma and pro forma as adjusted consolidated financial data, which gives effect to the transactions described in the footnotes to the table. The unaudited pro forma and pro forma as adjusted consolidated financial data is presented for informational purposes only and does not purport to represent what our consolidated results of operations or financial position actually would have been had the transactions reflected occurred on the dates indicated or to project our financial condition as of any future date or results of operations for any future period.

| Years Ended December 31, | Three Months Ended March 31, |

|||||||||||||||||||

| 2005 | 2006 | 2007 | 2007 | 2008 | ||||||||||||||||

| (unaudited) |

||||||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||||||||||

| Revenues: |

||||||||||||||||||||

| Product |

$ | 2,265 | $ | 2,544 | $ | 11,418 | $ | 1,456 | $ | 3,545 | ||||||||||

| Related party collaborative research and development |

| 863 | 8,481 | 1,289 | 3,881 | |||||||||||||||

| Collaborative research and development |

9,363 | 8,403 | 4,733 | 1,882 | 865 | |||||||||||||||

| Government grants |

156 | 317 | 701 | 77 | 83 | |||||||||||||||

| Total revenues |

11,784 | 12,127 | 25,333 | 4,704 | 8,374 | |||||||||||||||

| Cost and operating expenses: |

||||||||||||||||||||

| Cost of product revenues |

2,233 | 1,806 | 8,319 | 1,351 | 2,887 | |||||||||||||||

| Research and development |

12,839 | 17,257 | 35,644 | 4,763 | 9,855 | |||||||||||||||

| Selling, general and administrative |

7,891 | 11,880 | 19,713 | 4,036 | 8,738 | |||||||||||||||

| Total cost and operating expenses |

22,963 | 30,943 | 63,676 | 10,150 | 21,480 | |||||||||||||||

| Loss from operations |

(11,179 | ) | (18,816 | ) | (38,343 | ) | (5,446 | ) | (13,106 | ) | ||||||||||

| Interest income |

245 | 742 | 1,491 | 368 | 761 | |||||||||||||||

| Interest expense and other |

(413 | ) | (724 | ) | (2,533 | ) | 32 | (1,466 | ) | |||||||||||

| Loss before provision (benefit) for income taxes |

(11,347 | ) | (18,798 | ) | (39,385 | ) | (5,046 | ) | (13,811 | ) | ||||||||||

| Provision (benefit) for income taxes |

243 | (127 | ) | (408 | ) | 50 | 98 | |||||||||||||

| Net loss |

$ | (11,590 | ) | $ | (18,671 | ) | $ | (38,977 | ) | $ | (5,096 | ) | $ | (13,909 | ) | |||||

| Net loss per share of common stock, basic and diluted(1) |

$ | (7.69 | ) | $ | (10.99 | ) | $ | (15.53 | ) | $ | (2.72 | ) | $ | (4.10 | ) | |||||

| Shares used in computing net loss per share of common stock, basic and diluted(1) |

1,508 | 1,699 | 2,510 | 1,873 | 3,395 | |||||||||||||||

| Pro forma net loss per share of common stock, basic and diluted (unaudited)(1) |

$ | (1.29 | ) | $ | (0.37 | ) | ||||||||||||||

| Shares used in computing the pro forma net loss per share of common stock, basic and diluted (unaudited)(1) |

29,116 | 35,725 | ||||||||||||||||||

| (1) | Please see Note 2 of our consolidated financial statements appearing elsewhere in this prospectus for an explanation of the method used to calculate basic and diluted net loss per share of common stock, the pro forma basic and diluted net loss per share of common stock and the number of shares used in the computation of the per share amounts. |

7

Table of Contents

| March 31, 2008 | |||||||||

| Actual | Pro Forma(1) | Pro Forma As Adjusted(2)(3) |

|||||||

| (unaudited) | (unaudited) | ||||||||

| (in thousands) | |||||||||

| Consolidated Balance Sheet Data: |

|||||||||

| Cash, cash equivalents and marketable securities |

$ | 64,912 | $ | 64,912 | |||||

| Working capital |

42,404 | 44,664 | |||||||

| Total assets |

95,197 | 95,197 | |||||||

| Preferred stock warrant liability |

2,260 | | |||||||

| Current and long-term financing obligations |

16,889 | 16,889 | |||||||

| Redeemable convertible preferred stock |

132,746 | | |||||||

| Stockholders (deficit) equity |

(100,139 | ) | 34,867 | ||||||

| (1) | The pro forma data gives effect to (i) conversion of all of our outstanding shares of redeemable convertible preferred stock into shares of common stock, and (ii) conversion of all of our warrants for redeemable convertible preferred stock into warrants for common stock and the related reclassification of preferred stock warrant liability to stockholders equity upon the completion of this offering. |

| (2) | The pro forma as adjusted balance sheet data gives effect to the sale of shares of common stock in this offering at the initial public offering price of $ per share, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| (3) | Each $1.00 increase or decrease in the assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus) would increase or decrease, as applicable, our cash, cash equivalents and marketable securities, working capital, total assets and stockholders deficit by approximately $ million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

8

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as the other information in this prospectus, before deciding whether to invest in shares of our common stock. The occurrence of any of the events described below could harm our business, financial condition, results of operations and growth prospects. In such an event, the trading price of our common stock may decline and you may lose all or part of your investment.

Risks Relating to Our Business

We have a limited operating history, which may make it difficult to evaluate our current business and predict our future performance.

Our company has been in existence since 2002. Our operations to date have been primarily limited to organizing and staffing our company, developing our technology platform and establishing arrangements with customers, contract manufacturers and collaborators. Consequently, any assessments of our current business and predictions you make about our future success or viability may not be as accurate as they could be if we had a longer operating history. We have encountered and will continue to encounter risks and difficulties frequently experienced by growing companies in rapidly changing industries. If we do not address these risks successfully, our business will be harmed.

Our quarterly operating results may fluctuate in the future. As a result, we may fail to meet or exceed the expectations of research analysts or investors, which could cause our stock price to decline.

Our financial condition and operating results have varied significantly in the past and may continue to fluctuate from quarter to quarter and year to year in the future due to a variety of factors, many of which are beyond our control. Factors relating to our business that may contribute to these fluctuations include the following factors, as well as other factors described elsewhere in this prospectus:

| | our ability to achieve or maintain profitability; |

| | our ability to manage our growth; |

| | our ability to remediate a material weakness and implement effective internal controls; |

| | actions that could cause us to lose our licenses from Maxygen; |

| | our ability to maintain rights we have under our agreement with Maxygen; |

| | our relationships with collaborators; |

| | our dependence on key customers; |

| | our dependence on a limited number of contract manufacturers of our biocatalysts and suppliers for our pharmaceutical intermediates; |

| | our ability to develop and successfully commercialize products for the pharmaceuticals market; |

| | our ability to commercialize our technology in the biofuels and other bioindustrial markets; |

| | our ability to develop or obtain commercial scale expression systems for cellulases; |

| | risks associated with the international aspects of our business; |

| | potential issues related to our ability to accurately report our financial results in a timely manner; |

| | our dependence on and the need to attract and retain key personnel, including management; |

| | our ability to prevent the theft or misappropriation of our biocatalysts, the genes that code for our biocatalysts, know-how or technologies; |

9

Table of Contents

| | our ability to obtain, protect and enforce our intellectual property rights; |

| | our reliance on third parties to enforce patents for which we hold a license; |

| | potential advantages that our competitors may have in securing funding or developing products; and |

| | potential product liability claims, including claims relating to our use of hazardous materials. |

Due to the various factors mentioned above, and others, the results of any prior quarterly or annual periods should not be relied upon as indications of our future operating performance.

We have a history of net losses, and we may not achieve or maintain profitability.

We have incurred net losses since our inception, including losses of $11.6 million, $18.7 million and $39.0 million in 2005, 2006 and 2007, respectively. As of March 31, 2008, we had an accumulated deficit of $108.1 million. We expect to incur losses and negative cash flow from operating activities for the next several years. To date, we have derived a substantial portion of our revenues from research and development agreements with our collaborators and expect to derive a substantial portion of our revenue from these sources for at least the next several years. If we are unable to extend our existing agreements or enter into new agreements upon the expiration or termination of our existing agreements, our revenues could be adversely affected. In addition, some of our collaboration agreements provide for milestone payments and future royalty payments, the payment of which are uncertain as they are dependent on our and our collaborators abilities and willingness to successfully develop and commercialize products. We expect to spend significant amounts to fund the development of additional pharmaceutical and potential bioindustrial products, including biofuels. As a result, we expect that our operating expenses will exceed revenues for the next several years and we do not expect to achieve profitability during that period, if ever. If we fail to achieve profitability, or if the time required to achieve profitability is longer than we anticipate, we may not be able to continue our business. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis.

If our existing collaboration agreements expire or are terminated, our revenues could be adversely affected.

Our existing collaboration agreements generally have fixed terms and may be terminated under certain conditions. Accordingly, our ability to derive revenue from collaborations following the expiration or termination of these arrangements is uncertain, and will depend in large part on our ability to either extend existing collaborations or enter into new collaborative arrangements. Our ability to do so will, in turn, be largely dependent on our ability to address the needs of current and potential future collaborators.

We may continue to encounter difficulties managing our growth, which could adversely affect our business.

Our business has grown rapidly and we expect this growth to continue. Overall, we have grown from approximately 40 employees at the end of 2002 to approximately 253 employees as of March 31, 2008. Currently we are working simultaneously on multiple projects targeting several markets. Furthermore, we are conducting our business across several countries, including activities in the United States, Singapore, Hungary, Germany and India. These diversified, global operations place increased demands on our limited resources and require us to substantially expand the capabilities of our administrative and operational resources and to attract, train, manage and retain qualified management, technicians, scientists and other personnel. As our operations expand domestically and internationally, we will need to continue to manage multiple locations and additional relationships with various customers, collaborators, suppliers and other third parties. Our ability to manage our operations, growth, and various projects effectively will require us to make additional investment in our infrastructure to continue to improve our operational, financial and management controls and our reporting systems and procedures and to attract and retain sufficient numbers of talented employees, which we may be unable to do. As a result, we may be unable to manage our expenses in the

10

Table of Contents

future, which may negatively impact our gross margins or operating expenses in any particular quarter. In addition, we may not be able to successfully improve our management information and control systems, including our internal control over financial reporting, to a level necessary to manage our growth and to remediate an existing material weakness in our internal control, and we may discover additional deficiencies in existing systems and controls that we may not be able to remediate in an efficient or timely manner.

We and our independent registered public accounting firm identified a material weakness in our internal control over financial reporting. If we fail to remediate this material weakness or are unable to maintain effective internal control over financial reporting in the future, the accuracy and timeliness of our financial reporting may be adversely affected.

In connection with the audit of our consolidated financial statements for 2005, 2006 and 2007, we and our independent registered public accounting firm identified a material weakness in our internal control over financial reporting. The material weakness we identified comprises (i) our lack of policies and procedures, with the associated internal controls, to appropriately address complex, non-routine transactions and (ii) the lack of a sufficient number of qualified personnel to timely account for such transactions in accordance with U.S. generally accepted accounting principles. The evidence of this material weakness included: improper revenue recognition for certain complex revenue arrangements; incorrect application of accounting standards for, and untimely communication of information relating to, certain stock option grants; the failure to identify pre-existing accounting issues and control deficiencies at two acquired companies and the incorrect assessment of fair value of certain acquired tangible assets; the improper recording of cumulative foreign currency translation adjustments, resulting in part from our selection of the incorrect functional currency for a foreign subsidiary; and the lack of effective inventory management processes, primarily relating to the segregation of research and development materials from commercial inventories. The material weakness resulted in the recording of numerous audit adjustments, and significantly delayed our financial statement close process, for the three-year period ended December 31, 2007 and the three-month period ended March 31, 2008.

We have not yet been able to remediate this material weakness. However, we plan to take significant steps intended to address the underlying causes of the material weakness in the immediate future, primarily through the hiring of additional accounting and finance personnel with technical accounting and financial reporting experience, and the development and implementation of formal policies, improved processes and documented procedures. We do not know the specific timeframe needed to remediate all of the control deficiencies underlying this material weakness. In addition, we expect to incur significant incremental costs associated with this remediation, primarily due to the hiring of additional finance and accounting personnel, the retention of third-party experts and contractors, and the procurement, implementation and validation of robust accounting and financial reporting systems. If we fail to enhance our internal controls to meet the demands that will be placed upon us as a public company, including the requirements of the Sarbanes-Oxley Act of 2002, we may be unable to accurately report our financial results, or report them within the timeframes required by law or exchange regulations. We cannot assure you that we will be able to remediate this material weakness in a timely manner, if at all, or that in the future additional material weaknesses or significant deficiencies will not exist or otherwise be discovered, a risk that is significantly increased in light of the complexity of our business and multinational operations, and the emerging need for complex inter-subsidiary transactions. If our efforts to remediate the weakness identified are not successful or if other deficiencies occur, our ability to accurately and timely report our financial position, results of operations or cash flows could be impaired, which could result in late filings of our annual and quarterly reports under the Exchange Act, restatements of our consolidated financial statements, a decline in our stock price, suspension or delisting of our common stock by The Nasdaq Global Market, or other material effects on our business, reputation, results of operations, financial condition or liquidity.

11

Table of Contents

If we lose our licenses from Maxygen, we may be unable to continue our business.

We have licensed our core enabling intellectual property rights and technology from Maxygen, Inc., or Maxygen, under our March 2002 license agreement with Maxygen, which was subsequently amended in September 2002, October 2002, and August 2006. We rely heavily on this technology, which comprises advanced biotechnology methods, bioinformatics and years of accumulated know-how, to develop the optimized biocatalysts that are central to our business. Under the terms of the license agreement, we are obligated, among other things, to pay Maxygen a significant percentage of certain types of consideration we receive in connection with our biofuels research collaboration with Shell. During 2006 and 2007, as a result of consideration received in connection with this collaboration, we were obligated to pay Maxygen $0.6 million and $7.8 million, respectively. Maxygen has the right to terminate our rights under the agreement with respect to fuels, but not with respect to chemicals or pharmaceuticals, if we breach our royalty obligations to Maxygen and do not cure such breach within 60 days after we receive notice. Maxygen also has the right to terminate our license if we breach any third party agreements under which Maxygen sublicensed rights under the agreement, and fail to cure such breach within the time period specified in such third party agreement. Maxygen also has the right to terminate our license with respect to any family of related patent applications if we fail to pay our share of costs for obtaining and maintaining a patent licensed to us by Maxygen more than three times within any three year period. If the agreement were terminated, then we would lose our rights to utilize the technology and intellectual property covered by that agreement to develop, manufacture and commercialize many of our products. This would have a material adverse impact on our financial condition, results of operations and growth prospects and could prevent us from continuing our business.

We are dependent on our collaborators, and our failure to successfully manage these relationships could prevent us from developing and commercializing many of our products and achieving or sustaining profitability.

Our ability to maintain and manage collaborations with key industry leaders in our markets is fundamental to the success of our business. We currently have license agreements, collaborative research agreements, supply agreements, and/or distribution agreements with numerous parties. We may have limited or no control over the amount or timing of resources that any collaborator may devote to our partnered products or collaborative efforts. Any of our collaborators may fail to perform their obligations as expected. These collaborators may breach or terminate their agreements with us or otherwise fail to conduct their collaborative activities successfully and in a timely manner. Further, our collaborators may not develop products arising out of our collaborative arrangements or devote sufficient resources to the development, manufacture, marketing, or sale of these products. Moreover, disagreements with a collaborator could develop and any conflict with a collaborator could reduce our ability to enter into future collaboration agreements and negatively impact our relationships with one or more existing collaborators. If any of these events occur, or if we fail to maintain our agreements with our collaborators, we may not be able to commercialize our existing and potential products, grow our business, or generate sufficient revenue to support our operations. Our collaboration opportunities could be harmed if:

| | we do not achieve our research and development objectives under our collaboration agreements in a timely manner or at all; |

| | we develop products and processes or enter into additional collaborations that conflict with the business objectives of our other collaborators; |

| | we disagree with our collaborators as to rights to intellectual property we develop, or their research programs or commercialization activities; |

| | we are unable to manage multiple simultaneous collaborations; |

| | our collaborators become competitors of ours or enter into agreements with our competitors; |

12

Table of Contents

| | our collaborators become less willing to expend their resources on research and development or commercialization efforts due to general market conditions or other circumstances beyond our control; or |

| | consolidation in our target markets limits the number of potential collaborators. |

Additionally, our business could be negatively impacted if any of our collaborators or suppliers undergoes a change of control or were to otherwise assign the provisions of any of our agreements. For example, under our license agreement with Shell, Shell may assign the agreement without our consent in connection with a change of control. If Shell or any of our other collaborators were to assign these agreements to a competitor of ours or to a third party who is not willing to work with us on the same terms or commit the same resources as the current collaborator, our business could be harmed.

Our future success is heavily dependent on our collaborative research agreement with Shell.

Our current business plan for biofuels is heavily dependent on our collaborative research agreement with Shell, which will continue to be critical to our success in researching and developing successful biocatalysts for producing biofuel products. Shells efforts in commercializing those products profitably will be critical to the success of our business plan for biofuels. If we are unable to successfully execute on the development of products for Shell, our ability to expand into other bioindustrial areas may be significantly impaired, which will materially and adversely affect our ability to grow our business.

A delay or failure in Shells performance under the collaborative research agreement or license agreement with us would have a material adverse effect on our business and financial condition. We cannot control Shells performance or the resources it devotes to our programs. For example, although Shell has agreed to fund a specified number of our full-time employee equivalents in the performance of activities under the collaborative research agreement, Shell has the right under various circumstances to decrease the number of our full-time employee equivalents that it supports. Any such reduction would have a material impact on our revenue and business plan for biofuels. Moreover, disputes may arise between us and Shell, which could delay the programs on which we are working or could prevent us from commercially exploiting our technology platform and any developments resulting from the collaborative research agreement. If that were to occur, we may have to use funds, personnel, equipment, facilities and other resources that we have not budgeted to undertake certain activities on our own. Performance issues, program delay or termination or unbudgeted use of our resources may have a material adverse effect on our business and financial condition. Even if we successfully develop commercially viable technologies, our ability to derive revenues from those technologies will be dependent upon Shells willingness and ability to commercialize them. Disagreements with Shell could also result in expensive arbitration or litigation, which may not be resolved in our favor. Shell could merge with or be acquired by another company or experience financial or other setbacks unrelated to our research collaboration agreement that could adversely affect us.

We have agreed to work exclusively with Shell until November 2012 in the field of converting cellulosic biomass into fermentable sugars that can be converted into fuels as well as the conversion of these sugars into fuels and related products. However, Shell is not required to work exclusively with us, and could develop or pursue alternative technologies that it decides to use for commercialization purposes instead of the technology developed under our collaborative research agreement with Shell. For example, Shell is currently working with Iogen to develop cellulosic ethanol and CHOREN Industries to develop biodiesels, and it recently announced a collaboration with Virent Energy Systems to develop biogasoline. If Shell does not pursue the commercialization of any cellulosic sugars, biofuels or related products that may be developed under our collaborative research agreement, our exclusive arrangement would prevent us from pursuing these opportunities with others and could place us at a significant competitive disadvantage in the biofuels market.

13

Table of Contents

We cannot guarantee that our relationship with Shell will continue. Shell can terminate its collaborative research agreement with us after November 1, 2009 for any or no reason by providing us with six months notice, and its license agreement with us for any or no reason by providing us with six months notice. Each party also has the right to terminate the license agreement and the collaborative research agreement in the case of an uncured breach by the other party, and to terminate the collaborative research agreement if that party believes the other party has assigned the collaborative research agreement to a direct competitor of the terminating party. If our collaboration with Shell were to fail, we would likely need to find another collaborator to provide the financial assistance and infrastructure necessary for us to develop and commercialize our products and execute our strategy with respect to biofuels. Failure to maintain this relationship would have a material adverse effect on our business, financial condition and prospects.

Our failure to enter into new collaborations in our target markets could prevent us from developing and commercializing many of our products and achieving or sustaining profitability.

In addition to our existing collaborations, we will need to enter into, maintain and manage additional collaborations in our target markets to continue to grow our business. Because we do not currently and may never possess the resources necessary to independently develop and commercialize all of the potential products that may result from our technologies, the growth and success of our business depends on our ability to continue to enter into, and derive additional revenue from, collaboration agreements to develop and commercialize potential products in our various target markets. If we are unable to enter into additional collaboration agreements on terms satisfactory to us, we may not be able to commercialize our existing and potential products, grow our business, or generate sufficient revenue to support our operations.

We are dependent on a limited number of customers.

Our current revenues are derived from a limited number of key customers. For the year ended December 31, 2007, our top five customers accounted for approximately 65% of our revenues, with Shell and Pfizer accounting for approximately 33% and 13%, respectively. For the three months ended March 31, 2008, our top five customers accounted for approximately 70% of our revenues, with Shell accounting for 46% of our revenues. We expect a limited number of customers to continue to account for a significant portion of our revenues for the foreseeable future. This customer concentration increases the risk of quarterly fluctuations in our revenues and operating results. The loss or reduction of business from one or a combination of our significant customers could adversely affect our revenues, financial condition and results of operations.

Our dependence on contract manufacturers for biocatalyst production exposes our business to risks.

We have limited internal capacity to manufacture biocatalysts and are unable to do so for commercial scale production. As a result, we are dependent upon the performance and capacity of third party manufacturers for the commercial scale manufacturing of our biocatalysts.

We have historically relied on one Italian contract manufacturer, CPC Biotech srl, or CPC, to manufacture substantially all of our commercial enzymes used in our pharmaceutical business. Our pharmaceutical business, therefore, faces risks of difficulties with, and interruptions in, performance by CPC, the occurrence of which could adversely impact the availability, launch and/or sales of our enzymes in the future. We are in the process of qualifying other contract manufacturers, but we do not have agreements or commitments with such contract manufacturers at this time. The failure of CPC or any other manufacturers that we may use to supply manufactured product on a timely basis or at all, or to manufacture our enzymes or other biocatalysts in compliance with our specifications or applicable quality requirements, or to manufacture our enzymes or other biocatalysts in volumes sufficient to meet demand would adversely affect our ability to achieve development milestones under our collaborations or sell our pharmaceutical products, could harm our relationships with our collaborators or customers and could negatively affect our revenues and operating results.

14

Table of Contents

We do not currently have a long-term supply contract with CPC or any other contract manufacturers, who are under no obligation to manufacture our enzymes and could elect to discontinue the manufacture of our enzymes at any time and without cause. If CPC does not expand its facilities to match our growing demand or if we are unable to contract with other manufacturers on commercially reasonable terms or at all, we will not have enough capacity to meet our current demand projections. If we require additional manufacturing capacity and are unable to obtain it in sufficient quantity, we may not be able to increase our pharmaceutical sales, or we may be required to make very substantial capital investments to build that capacity or to contract with another manufacturer on terms that may be less favorable than the terms we currently have with CPC. If we choose to build our own additional manufacturing capacity, it could take a year or longer before that facility is able to produce commercial volumes of our biocatalysts. In addition, if we contract with other manufacturers, we may experience delays of several months in qualifying them, which could harm our relationships with our collaborators or customers and could negatively affect our revenues or operating results.

We plan to evaluate whether to invest in our own manufacturing capabilities or to establish long-term supply contracts with additional contract manufacturers. However, we cannot guarantee that we will be able to acquire, develop or contract for internal manufacturing capabilities on commercially reasonable terms, or at all. Any resources we expend on acquiring or building internal manufacturing capabilities could be at the expense of other potentially more profitable opportunities.

We are primarily dependent on contract manufacturers to manufacture our pharmaceutical products.

We currently rely on a small number of collaborators and contract manufacturers to manufacture our pharmaceutical intermediates. For example, our collaborator Arch Pharmalabs Limited, or Arch, supplies us and our customers with intermediates manufactured using our proprietary biocatalysts.

Our pharmaceutical business faces risks of difficulties with, and interruptions in, performance by Arch, the occurrence of which could adversely impact the availability, launch and/or sales of our products in the future. The failure of Arch to supply intermediates on a timely basis or at all, or to manufacture our products in compliance with our specifications or applicable quality requirements, or to manufacture the product in volumes sufficient to meet demand would adversely affect our ability to commercialize our pharmaceutical products and could negatively affect our revenues and operating results. If Arch does not expand its facilities to match our growing demand, or experiences delays related to the construction of new facilities or the expansion of existing facilities, or if we are unable to contract with other suppliers on commercially reasonable terms or at all, we will not have enough capacity to meet our current demand projections.

We intend to use Arch as the primary supplier for our planned launch of APIs. We will rely on Arch to deliver materials on a timely basis and to comply with applicable regulatory requirements, which may include current Good Manufacturing Practices, or cGMP, and will be dependent on Arch to timely manufacture and deliver sufficient quantities of materials produced under cGMP conditions to enable us to bring products to market in a timely manner. Failure by Arch, or any other contract manufacturer that we rely on to manufacture APIs, to comply with applicable regulations could adversely affect the production and commercialization of API products, which could lead to lost sales. We also rely, to a lesser extent, on other contract manufacturers to supply our pharmaceutical intermediates. The failure of these manufacturers to supply intermediates, or to manufacture products in compliance with our specifications or in sufficient volumes, would have similar negative effects on our revenues and operating results.

15

Table of Contents

If we are unable to develop and commercialize new products for the generic pharmaceutical market, our business and prospects will be harmed.

We plan to launch several new intermediates and APIs for generic drugs in non-regulated markets, and plan to launch these same products in the regulated markets when the patent protection for each branded product expires. This effort is subject to numerous risks, including the following:

| | we may be unable to successfully develop the biocatalysts or manufacturing processes for our intermediates and APIs in a timely and cost-effective manner, if at all; |

| | we may face difficulties in transferring the developed technologies to Arch, or other contract manufacturers that we may use, for commercial scale production; |

| | Arch, or other contract manufacturers that we may use, may be unable to scale their manufacturing operations to meet the demand for these products and we may be unable to secure additional manufacturing capacity; and |

| | generics manufacturers may not be willing to purchase these products from us on favorable terms, if at all. |

If one or more of these risks were to materialize, our future business, results of operations and financial condition could be materially adversely affected, and we may be unable to grow our business.

We will face numerous risks relating to any pharmaceutical products that we commercialize.

The commercialization of pharmaceutical intermediates and APIs will expose us to a number of risks, including risks related to product liability litigation, unexpected safety or efficacy concerns, product recalls or withdrawals, changes in laws or regulations relating to the generics industry, negative publicity affecting doctor or patient confidence in the products, and pressure from existing or new competitive products. In addition, our existing and potential innovator customers may view us as competitors and be less willing to do business with us. Moreover, we may be subject to claims alleging that our pharmaceutical products violate the patent or other intellectual property rights of third parties, particularly in connection with any generic products on which the patent covering the branded drug is expiring. These claims could give rise to litigation, which may be costly and time-consuming and could divert managements attention. If we are unsuccessful in our defense of any such claims, we may lose our right to develop or manufacture the products, be required to pay monetary damages, or be required to enter into license agreements and pay substantial royalties. The occurrence of any of these events could have a material adverse effect on our business, results of operation, financial condition and cash flows.

Our business could be adversely affected if the clinical trials being conducted by our innovator customers who sell branded drugs fail or if the processes used by those customers to manufacture their final pharmaceutical products fail to be approved.

Our biocatalysts are used in the manufacture of intermediates and APIs which are then used in the manufacture of final pharmaceutical products by our customers who sell branded drugs, which we refer to as innovators. In order to sell these pharmaceutical products in markets that provide effective patent protection, which we refer to as regulated markets, the products must be approved by the FDA in the United States, and similar regulatory bodies in other regulated markets, prior to commercialization. If these customers experience adverse events in their clinical trials, fail to receive regulatory approval for the drugs, or decide for business or other reasons to discontinue their clinical trials or drug development activities, our revenues will be negatively impacted. The process of producing these drugs, and their generic equivalents, is also subject to regulation by the FDA in the United States and equivalent regulatory bodies in other regulated markets. If any pharmaceutical process that uses our biocatalysts does not receive approval by the appropriate regulatory body or if customers decide not to pursue approval, our business could be adversely affected.

16

Table of Contents

Our business could be adversely affected if customers do not adopt our processes.

Historically, pharmaceutical companies have been reluctant to use biocatalysts in the manufacture of their intermediates or APIs because naturally occurring biocatalysts were not economically viable for production at commercial scale. For example, naturally occurring biocatalysts are often not stable enough to be used in industrial settings. Additionally, the activity and productivity of these biocatalysts are often too limited to be effective in commercial scale manufacturing and often result in incomplete reactions and insufficient product yields. Although our biocatalysts have been developed to address these problems, we may still encounter reluctance by pharmaceutical companies to adopt processes that use our biocatalysts. If customers decide not to adopt processes using our biocatalysts over other methods of producing the intermediates or APIs for their drugs, our revenues will be negatively impacted.

Moreover, we believe that the lower manufacturing costs enabled by our technology platform is one of the principal reasons pharmaceutical companies have purchased and will continue to purchase our products and processes. If we are unable to maintain the cost advantages provided by our technology platform, customers may be less willing to acquire our products and processes, which would also negatively impact our revenues.

If we fail to fund research in certain areas, we will lose rights to develop products in those areas using technology licensed from Maxygen.

Under our license agreement with Maxygen, we can extend the scope of our license into several additional areas related to hydrogen, coal and natural gas-based fuels if we meet certain funding thresholds for research in those fields by September 2009. If we do not meet the funding requirements in any of those areas, we would lose our rights to use the licensed technology and intellectual property to develop products or pursue collaborations in that area, which could have a material adverse effect on our ability to grow our business and revenues.

We may need additional licenses from Maxygen to pursue certain future business opportunities in the chemical market.

Under our license agreement with Maxygen, we obtained exclusive rights to manufacture certain types of chemicals for specified purposes within particular fields. Should we desire to work on any chemicals that are outside the scope of these license rights, we may need to seek additional rights from Maxygen. Maxygen has no obligation to grant such rights to us and may choose not to license such rights to us on favorable terms, if at all. If we are unable to obtain rights to those additional areas, we may not be able to develop products or services or pursue collaborations in those areas, which could limit our ability to expand into the chemicals market.

Our government grants are subject to uncertainty, which could harm our business and results of operations.

We have received grants funded by various agencies of the federal government and foreign governments to complement and enhance our own resources. Funds available under these grants and contracts must be applied by us toward the research and development programs specified by the granting agencies rather than for all our programs generally. Moreover, revenues from such sources are uncertain because these agreements and grants generally have fixed terms and may be terminated, modified or recovered by the granting agency under certain conditions.

We may also be subject to audits by the government agencies as part of routine audits of our activities funded by our government grants. As part of an audit, these agencies may review our performance, cost structures and compliance with applicable laws, regulations and standards. If any of our costs are found to be allocated improperly, the costs may not be reimbursed and any costs already reimbursed for such

17

Table of Contents

contract may have to be refunded. Accordingly, an audit could result in an adjustment to our revenue and results of operations.

If we are unable to successfully commercialize our technology in biofuels and other bioindustrial markets, our business may fail to generate sufficient revenue, which would adversely affect our operating results.

We expect to derive a significant portion of our future revenue from the development of bioindustrial products, including biocatalysts for the production of biofuels, that we may develop with our collaborators, and by licensing our proprietary technology. In order to develop a viable biofuels business, we will need to demonstrate that we can develop biocatalysts that can be used to produce biofuels from cellulosic biomass. We do not know when we will be able to demonstrate these capabilities, if at all. If we are able to develop this technology, Shell has the right, but not the obligation, to commercialize this technology. If Shell decides to commercialize our technology, Shell will need to build a demonstration facility, design, finance and construct commercial scale biofuel facilities, and operate commercial scale facilities at costs that are competitive with traditional petroleum-based fuels and other alternative fuel technologies that may be developed.

In addition to biofuels, we expect to invest a significant amount of our future research and development efforts in other bioindustrial areas, including carbon management, water treatment and chemicals. We do not currently have any, and may be unable to secure, funded collaborations in these areas. Even if we are able to enter into collaborations in one or more of these areas, we and our collaborators may be unable to develop commercially viable solutions to these problems. Moreover, because we have limited financial and managerial resources, we will be required to prioritize our application of resources to particular development and commercialization efforts. Any resources we expend on one or more of these efforts could be at the expense of other potentially profitable opportunities. If we focus our efforts and resources on one or more of these areas and they do not lead to commercially viable products, our revenues, financial condition and results of operations could be adversely affected.

Production and commercialization of cellulosic biofuels and other chemicals derived from cellulose may not be feasible.

Production and commercialization of cellulosic biofuel products, and other chemicals derived from cellulose, may not be feasible for a variety of reasons. For example, the development of technology for converting sugar into a commercially viable non-ethanol biofuel alternative to petroleum-based fuels is still in its infancy, and we do not know whether this can be done commercially or at all. To date there has been a lack of significant private and government funding for research and development. Furthermore, there have been very few, if any, well-directed research and development public policies emphasizing investment in the research and development of, and providing incentives for the commercialization of, and transition to, biofuels.

Substantial development of infrastructure will be required for the biofuels industry to grow. Areas requiring expansion include, but are not limited to, additional rail capacity, additional storage facilities for biofuels, increases in truck fleets capable of transporting biofuels within localized markets, expansion of refining and blending facilities to handle biofuels, and growth in the fleet of vehicles capable of using biofuels. Substantial investments required for infrastructure changes and expansions may not be made on a timely basis or at all. Any delay or failure in making the changes to or expansion of infrastructure could harm demand or prices for potential biofuel products and impose additional costs that would hinder the commercialization of biofuels.

Currently, we believe that there are no commercial scale cellulosic biofuel production plants in operation in the United States. There can be no assurance that anyone will be able or willing to develop and operate biofuel production plants at commercial scale or that any biofuel facilities can be profitable.

18

Table of Contents